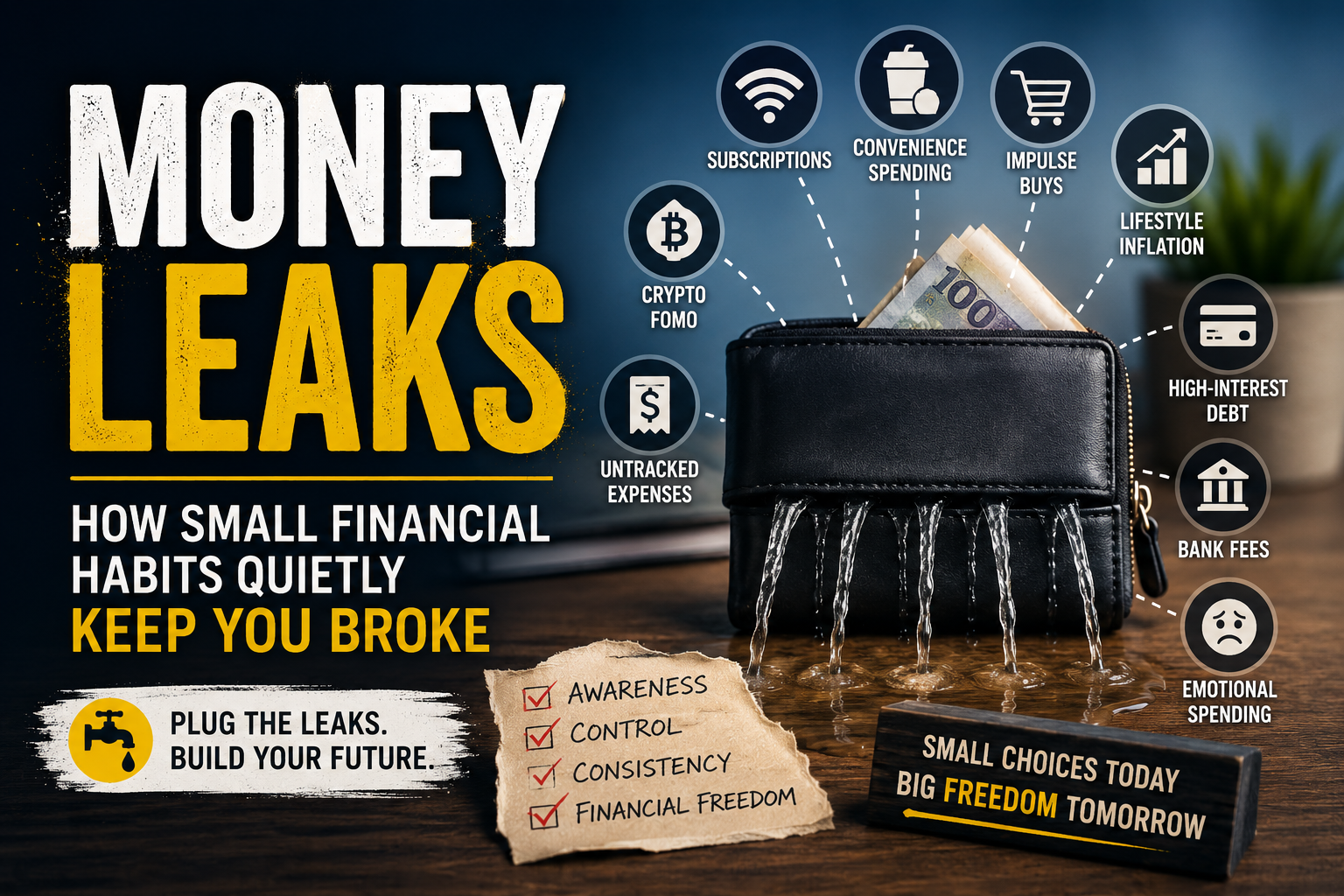

Money leaks are one of the quietest reasons people struggle to build wealth.

At first, they rarely look dramatic.

No one wakes up and says, “Today I am going to destroy my financial future with tiny spending habits.”

Instead, the damage usually happens in small moments.

A subscription renews. A delivery order feels convenient. One bank fee goes unnoticed. Another small impulse purchase does not seem serious. Later, a “quick” crypto trade becomes another avoidable loss. Then, after a salary increase, a lifestyle upgrade quietly becomes the new normal.

Individually, these choices may look harmless.

However, when they repeat every week and every month, they can drain the money that could have gone toward savings, investing, debt reduction, emergency funds, property, crypto, or passive income systems.

That is why this topic matters.

Building passive income requires capital. Consistent investing needs margin. Smart financial risks also depend on stability.

Unfortunately, money leaks reduce all three.

This article will help you identify the small financial habits that quietly keep you broke, understand why they happen, and build a practical system to plug the leaks without living a miserable life.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Personal finance decisions should be based on your own income, expenses, debt, goals, risk tolerance, and local regulations.

If you have not yet read the SPI guide on active income vs passive income, start there as well. That article explains how income systems are built. This guide focuses on protecting the money that can help you build those systems.

The Problem Is Not Always How Much You Earn

Many people assume their financial problem is only an income problem.

Sometimes, that is true.

A person may genuinely need to earn more because basic living costs are too close to their income. In that situation, increasing income becomes important.

Still, income is only one side of the equation.

The other side is behaviour.

Someone can earn more money and still remain financially stressed if every income increase creates a new spending increase. As a result, some people get salary increases but never feel wealthier.

The extra money arrives, then disappears.

Often, that disappearing money is caused by money leaks.

A money leak is any repeated financial habit, fee, expense, or decision that slowly drains your financial progress without giving you enough value in return.

These leaks are dangerous because they feel small in the moment.

Over time, though, small leaks can become large losses.

What Is a Money Leak?

A money leak is not the same as normal spending.

Spending money is part of life. You need food, transport, shelter, communication, healthcare, education, family support, and enjoyment.

The problem begins when money leaves your life without a clear purpose, plan, or value.

For example, paying for a useful subscription you use every week may be reasonable. By contrast, paying for five subscriptions you forgot about is a leak.

Buying a takeaway meal occasionally may be fine. However, ordering food because you never planned groceries can become a leak.

Owning a car may be necessary. Yet upgrading vehicles every time your income improves can turn into a lifestyle leak.

Crypto investing can also fit into a broader strategy. On the other hand, jumping into every trending coin because of fear of missing out is often a leak disguised as opportunity.

The key question is simple:

Is this expense helping my life, or is it quietly weakening my financial future?

Why Money Leaks Are So Easy to Miss

Money leaks are easy to miss because they hide inside normal life.

Most people notice big financial decisions.

They notice buying a car. Rent or bond payments are also obvious. School fees, medical aid, large loan repayments, and insurance premiums usually stand out.

Small leaks work differently.

A R49 fee feels small. A R100 impulse buy feels manageable. One R200 delivery order feels like convenience. Meanwhile, a R300 subscription feels normal because it has been there for months.

Because each expense feels small, the brain does not treat it as a serious threat.

However, money does not care whether the leak felt small.

It only cares that it left your account.

| Small Leak | Monthly Cost | Yearly Cost |

|---|---|---|

| Unused subscription | R99 | R1,188 |

| Extra delivery fees | R300 | R3,600 |

| Impulse spending | R500 | R6,000 |

| Bank fees and penalties | R150 | R1,800 |

| Unplanned convenience spending | R700 | R8,400 |

None of those examples looks huge on its own.

Together, though, they can easily represent thousands of rand per year.

That money could have funded an emergency account, an ETF portfolio, a business idea, a digital product, debt repayment, or a carefully researched investment plan.

Money Leak 1: Unused Subscriptions

Subscriptions are one of the easiest money leaks to ignore.

Streaming services, apps, cloud storage, software, gym contracts, newsletters, mobile add-ons, trading tools, and platform memberships can slowly pile up.

At first, each one seems affordable.

Eventually, the total cost can become uncomfortable.

The real problem is not the subscription itself. Rather, the problem is paying for something that no longer serves you.

A useful subscription can save time, improve your work, educate you, entertain you, or support your business. In that case, it may be worth keeping.

A forgotten subscription is different.

That is money leaving your account without a current purpose.

How to Plug This Leak

- Check your bank statement for recurring payments.

- Cancel anything you have not used in the last 30 days.

- Downgrade plans that are bigger than what you need.

- Set a reminder before free trials become paid subscriptions.

- Review subscriptions every three months.

This one exercise can free up money quickly.

More importantly, it teaches you to question automatic spending.

Money Leak 2: Convenience Spending

Convenience spending is not always bad.

Sometimes paying for convenience is reasonable. A busy parent, business owner, student, or professional may need to save time.

Still, convenience becomes a leak when it replaces basic planning.

Food delivery is a common example.

The meal itself may not be the only cost. Delivery fees, service fees, tips, markups, and impulse add-ons can increase the total.

Another example is buying items at the nearest expensive store because you did not plan ahead.

Once or twice, this may not matter.

Repeated every week, it becomes expensive.

How to Plug This Leak

- Plan simple meals for the week.

- Keep quick backup meals at home.

- Set a monthly convenience spending limit.

- Use delivery intentionally, not automatically.

- Compare the full cost, including fees.

The goal is not to remove all comfort from your life.

Instead, the goal is to stop convenience from silently controlling your budget.

Money Leak 3: Lifestyle Inflation

Lifestyle inflation happens when your spending rises every time your income rises.

A salary increase feels good.

At first, you may plan to save more, invest more, or pay off debt faster.

Then life adjusts.

A better phone appears. A nicer car seems reasonable. Restaurants become more frequent. Clothes become more expensive. Holidays become bigger. Monthly commitments increase.

Eventually, the new income feels normal.

At that point, the opportunity is gone.

Lifestyle inflation is dangerous because it can make higher income feel useless.

You earn more, but your financial position does not improve.

How to Plug This Leak

- Decide in advance what percentage of any income increase will be saved or invested.

- Upgrade slowly instead of upgrading everything at once.

- Avoid adding permanent expenses after temporary excitement.

- Use salary increases to reduce debt or build assets first.

- Keep your lifestyle below your income growth.

One practical rule is simple:

When income increases, upgrade your financial future before upgrading your lifestyle.

Money Leak 4: High-Interest Debt

High-interest debt is one of the most damaging money leaks.

Credit cards, store accounts, payday loans, personal loans, and short-term credit can become expensive when balances are carried for too long.

The problem is that interest does not sleep.

While you are trying to save or invest, high-interest debt may be working against you in the background.

That creates a painful situation.

Your investments may need to work extremely hard just to beat the interest you are paying elsewhere.

South African readers who are struggling with debt can learn more about debt counselling through the National Credit Regulator. The NCR explains that debt counselling is intended to assist over-indebted consumers through budget advice and negotiations with credit providers. You can read more here: NCR: Debt Counselling.

How to Plug This Leak

- List every debt, balance, interest rate, and minimum payment.

- Prioritise high-interest debt first where possible.

- Avoid taking new debt to fund lifestyle spending.

- Pay more than the minimum when you can.

- Seek professional help if debt feels unmanageable.

Debt repayment may not feel exciting.

Even so, reducing high-interest debt can be one of the strongest financial moves a beginner can make.

Money Leak 5: Bank Fees and Penalties

Bank fees can be sneaky.

Monthly account fees, withdrawal fees, failed debit order fees, overdraft charges, international transaction fees, and penalty fees can quietly reduce your money.

Some fees may be unavoidable.

Others can be reduced with better account choices and habits.

For example, using the wrong account type for your behaviour can cost more than necessary. Frequent cash withdrawals, failed payments, and unnecessary account features may add up over time.

How to Plug This Leak

- Review your bank charges monthly.

- Compare account types at your bank.

- Avoid failed debit orders where possible.

- Use digital payments when cheaper.

- Keep a small buffer to avoid accidental overdraft costs.

Bank fees may not disappear completely.

However, understanding them gives you more control.

Money Leak 6: Emotional Spending

Emotional spending happens when money becomes a response to stress, boredom, sadness, pressure, or excitement.

Sometimes it looks like retail therapy.

Other times, it sounds like “I deserve this” spending after a difficult week.

Occasional treats are not the problem.

The leak begins when spending becomes your main emotional coping tool.

That pattern can become expensive because the purchase may only give short-term relief.

Afterwards, the financial stress returns.

In some cases, it becomes worse.

How to Plug This Leak

- Use a 24-hour waiting rule before non-essential purchases.

- Keep a separate “fun money” budget.

- Write down what triggered the urge to spend.

- Find low-cost ways to relax or reset.

- Avoid shopping apps when emotional.

The goal is not to remove enjoyment.

Instead, the goal is to stop emotions from making financial decisions without your permission.

Money Leak 7: Crypto FOMO

Crypto FOMO is one of the most dangerous leaks for people interested in digital assets.

FOMO means fear of missing out.

In crypto, it often appears when a coin is pumping, a group chat is excited, an influencer is confident, or screenshots of profits are everywhere.

Suddenly, research disappears.

The decision becomes emotional.

A person buys because they do not want to feel left behind.

That can turn into a financial leak very quickly.

Crypto is already volatile. Adding emotional decision-making makes it even riskier.

SPI has covered this in more detail in the guides on crypto bull market mistakes, exit liquidity in crypto, and crypto project vetting checklist.

How to Plug This Leak

- Do not buy only because a price is moving fast.

- Use a research checklist before entering any project.

- Set a maximum risk amount before emotions rise.

- Avoid chasing screenshots from other people.

- Take time to understand the project, tokenomics, liquidity, and risks.

Crypto opportunities can be real.

Nevertheless, FOMO is not a strategy.

Money Leak 8: Not Tracking Where Money Goes

Many people do not have a clear picture of where their money goes.

They know their salary.

Rent or bond payments may also be clear.

A few big expenses are easy to remember.

After that, things become blurry.

This is where leaks hide.

Without tracking, you may underestimate food costs, transport, subscriptions, entertainment, impulse purchases, bank fees, and debt charges.

Financial education matters because it improves decision-making. The OECD explains financial literacy as awareness, knowledge, skills, attitudes, and behaviours that support informed financial decisions. You can read more here: OECD: Financial Education.

How to Plug This Leak

- Track every expense for 30 days.

- Group spending into categories.

- Identify the top three leaks.

- Set realistic limits for weak areas.

- Review your progress weekly.

Tracking is not about guilt.

It is about visibility.

You cannot fix what you cannot see.

Money Leak 9: Spending Before Saving

Many people save whatever is left at the end of the month.

The problem is that there is often nothing left.

Life has a way of using available money.

If saving and investing come last, they are easy to skip.

A stronger approach is to treat saving as a planned expense.

This does not mean you need to save huge amounts immediately.

Even a small automatic transfer can build the habit.

How to Plug This Leak

- Set an automatic transfer after payday.

- Start with a realistic amount.

- Increase the amount when income improves.

- Keep savings separate from spending money.

- Give each savings goal a clear purpose.

Investor.gov offers a compound interest calculator that shows how contributions, time, and returns can affect long-term growth. You can use it here: Investor.gov Compound Interest Calculator.

Small amounts can matter when they become consistent.

Money Leak 10: Buying Cheap Repeatedly

Buying the cheapest option can sometimes save money.

Other times, it creates a leak.

Cheap items that break quickly may need to be replaced again and again. Over time, the “cheap” option becomes more expensive than buying better quality once.

This applies to clothing, electronics, tools, appliances, furniture, shoes, and even business equipment.

The lesson is not to buy expensive things for status.

Rather, the lesson is to think about cost per use.

How to Plug This Leak

- Ask how often you will use the item.

- Compare durability, not only price.

- Read reviews before buying.

- Avoid replacing the same low-quality item repeatedly.

- Spend more only when quality truly matters.

Sometimes the cheaper option is smart.

Sometimes it is just a delayed expense.

Money Leak 11: Poor Planning That Creates Emergency Spending

Some emergencies are real and unavoidable.

Others are predictable expenses that were not planned for.

Car maintenance, school costs, annual renewals, medical expenses, home repairs, birthdays, travel, insurance excesses, and appliance replacements can all surprise people who do not plan ahead.

When these costs arrive, many people use debt.

That turns poor planning into a bigger financial problem.

How to Plug This Leak

- Create sinking funds for predictable expenses.

- Review annual costs at the start of the year.

- Keep a basic emergency fund.

- Plan for maintenance before things break.

- Separate true emergencies from predictable expenses.

A sinking fund is simply money set aside for a known future cost.

That small habit can reduce stress and protect you from unnecessary debt.

Money Leak 12: Mistaking Affordability for Wisdom

One of the most dangerous phrases in personal finance is:

“I can afford it.”

Being able to pay for something does not automatically make it a wise decision.

You may be able to afford a monthly payment, but that does not mean the item supports your goals.

You may be able to afford a new phone, but your current one may still work.

A car upgrade may fit into your monthly budget, but it could delay investing, debt repayment, or emergency savings.

Affordability looks at whether you can pay.

Wisdom asks whether you should.

How to Plug This Leak

- Ask what the purchase will delay.

- Compare the item with your bigger goals.

- Think beyond the monthly payment.

- Include insurance, maintenance, fees, and opportunity cost.

- Wait before making lifestyle upgrades.

Opportunity cost matters.

Every rand used in one place cannot be used somewhere else.

The Money Leak Audit

A money leak audit is a simple process for finding where your money escapes.

You do not need complicated software.

A notebook, spreadsheet, budgeting app, or bank statement can work.

The goal is to see your money clearly.

| Step | Action | Purpose |

|---|---|---|

| Step 1 | Review 30 to 90 days of transactions | Find repeated spending patterns |

| Step 2 | Highlight unused or low-value expenses | Identify easy cuts |

| Step 3 | Group spending by category | See where money actually goes |

| Step 4 | Choose the top three leaks | Focus on meaningful improvements |

| Step 5 | Redirect saved money | Turn leaks into progress |

Finally, the last step is the most important.

Do not only cut expenses.

Redirect the money.

If you cancel a R200 subscription, send that R200 somewhere useful. It could go toward debt, an emergency fund, ETFs, education, business tools, or another goal.

Otherwise, the money may leak somewhere else.

Where the Saved Money Should Go

Plugging money leaks is powerful, but only if the recovered money gets a job.

That job depends on your current financial stage.

| Financial Situation | Possible Priority |

|---|---|

| No emergency fund | Build a small safety buffer |

| High-interest debt | Reduce expensive debt |

| Stable basics | Start consistent investing |

| Interested in passive income | Build capital for income-producing assets |

| Crypto investor | Improve research, risk control, and profit planning |

This is where money leaks connect directly to passive income.

Every leak you plug can become fuel for an income system.

That system might be an ETF portfolio, a rental property plan, a digital product, a newsletter, a business idea, or a carefully researched crypto strategy.

Related SPI reads:

- Passive Income Ideas for Beginners

- Active Income vs Passive Income

- Best ETFs for Beginners in 2026

- Crypto Profit-Taking Strategy

How to Fix Money Leaks Without Feeling Restricted

Many people avoid budgeting because they think it means punishment.

That mindset makes financial improvement harder than it needs to be.

Plugging money leaks is not about removing all enjoyment.

Instead, it is about spending with intention.

You can still enjoy life. Eating out, buying nice things, supporting family, and entertainment can still have a place.

The difference is that your spending should match your values and goals.

A simple system can help:

- Protect essentials first.

- Automate saving or debt repayment.

- Give yourself guilt-free spending money.

- Review leaks once a month.

- Increase investing as income grows.

This approach is more sustainable than extreme restriction.

People rarely stick with a plan that makes life feel miserable.

A good money system should create control, not constant stress.

Final Thoughts

Money leaks are easy to ignore because they rarely feel serious in the moment.

However, repeated small leaks can quietly weaken your financial future.

Unused subscriptions, convenience spending, lifestyle inflation, bank fees, emotional purchases, high-interest debt, poor planning, and crypto FOMO can all drain money that could have built something meaningful.

The solution is not to live with fear or guilt.

Instead, the solution is awareness.

Find the leaks. Understand why they happen. Plug the biggest ones first. Then redirect the saved money toward something that improves your future.

That might be debt freedom, emergency savings, investing, property, crypto research, a business idea, or a passive income system.

Small leaks can keep you stuck.

Small improvements can move you forward.

The difference is whether your money disappears by accident or gets used with purpose.

Start there.

That is how financial progress becomes practical.

Leave a Reply