DeFi lending protocols are one of the most important parts of crypto because they show how borrowing and lending can happen without a traditional bank controlling the middle.

Crypto Has Its Own Money Markets

When beginners first hear about crypto, they usually think about buying coins and waiting for the price to go up.

That is only one part of the story.

Behind the charts, crypto has its own financial infrastructure. There are stablecoins, decentralized exchanges, liquidity pools, bridges, staking systems, tokenized assets, and lending protocols.

DeFi lending protocols are one of the clearest examples of this infrastructure.

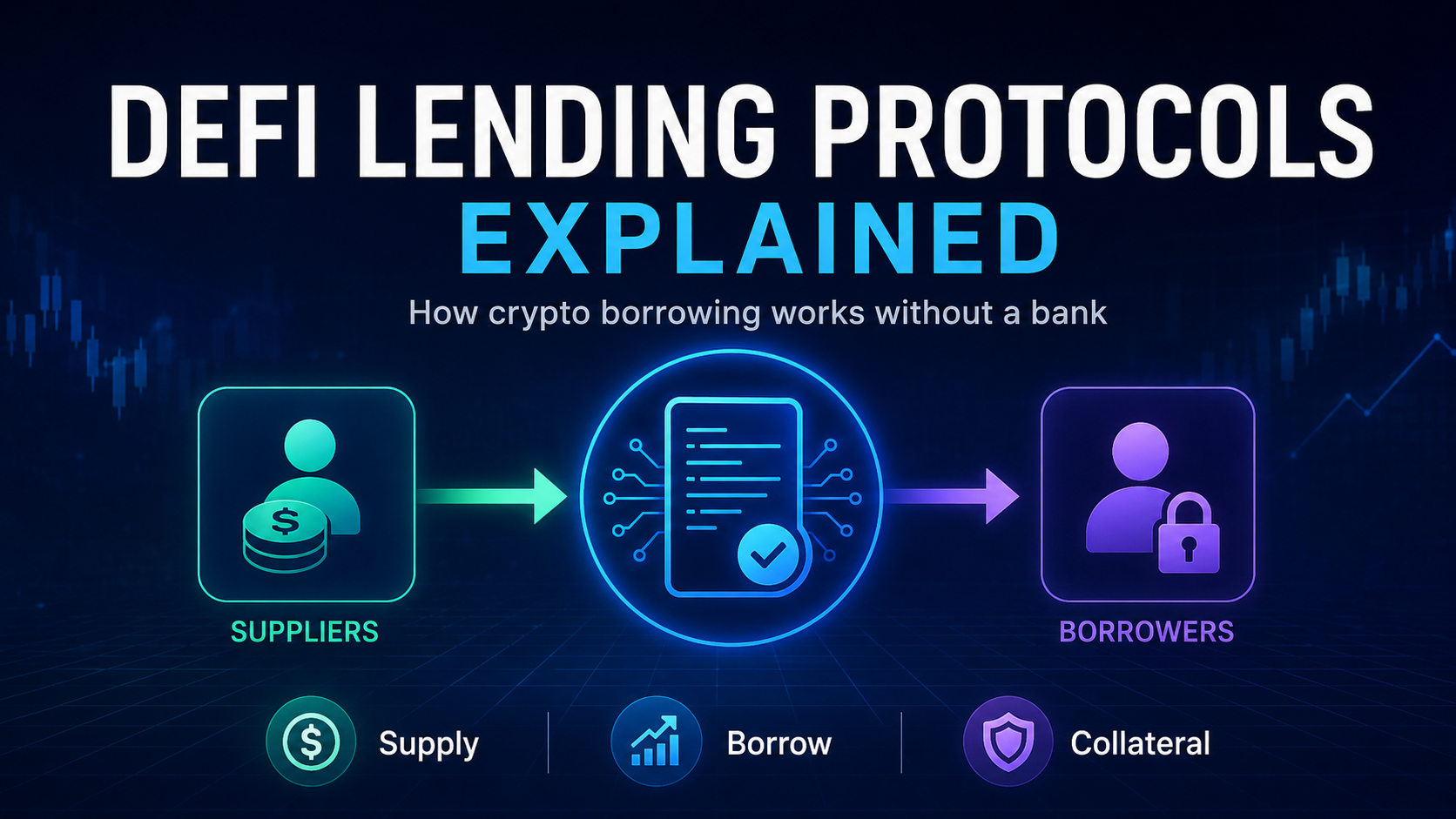

They allow people to supply crypto assets, borrow against collateral, repay loans, earn interest, and access liquidity through smart contracts instead of traditional bank branches.

That may sound technical at first, but the basic idea is not too difficult.

In a normal banking system, depositors place money in the bank, borrowers take loans, and the bank manages the middle.

In DeFi lending, users supply crypto into smart contracts, other users borrow from those markets, and collateral helps protect the system.

The bank is replaced by code, liquidity pools, collateral rules, price feeds, and liquidation systems.

This does not make DeFi perfect.

It simply makes it different.

If you want to understand crypto beyond price speculation, DeFi lending protocols are worth studying because they explain how crypto-native borrowing and lending works in practice.

This article also connects naturally with other Simple Passive Income guides, including the 10-Step DeFi Safety Checklist, Best On-Chain Crypto Tools, and Tokenized Real Estate for Beginners.

Those guides help readers think about research, safety, real-world assets, and crypto infrastructure. This guide focuses on one of DeFi’s core building blocks: lending.

What Are DeFi Lending Protocols?

DeFi lending protocols are blockchain-based systems that allow users to lend and borrow crypto assets through smart contracts.

In traditional finance, a bank or lender usually decides who qualifies for a loan.

The bank may check income, employment, debt, credit score, documents, and affordability. After that, the borrower signs legal agreements and repays according to the loan terms.

DeFi lending works differently.

Instead of asking who the borrower is, most DeFi lending protocols ask a different question:

Does the borrower have enough collateral?

This is the foundation of most DeFi lending.

A user supplies one asset as collateral and borrows another asset against it.

For example, someone may supply ETH as collateral and borrow USDC.

The protocol does not need to know the borrower’s job title, salary, address, or credit history. It mainly looks at the collateral value, the asset being borrowed, the lending rules, and whether the position remains healthy.

That is why DeFi lending is often described as overcollateralized lending.

Overcollateralized means the borrower usually deposits more value than they borrow.

This may feel strange at first because beginners often ask, “Why would I deposit R10,000 to borrow R5,000?”

The answer is simple: the borrower may not want to sell the asset they already own.

The Simple Bank vs DeFi Lending Comparison

To understand DeFi lending protocols, it helps to compare them with a normal bank loan.

| Feature | Traditional Bank Lending | DeFi Lending Protocols |

|---|---|---|

| Middleman | A bank or financial institution | Smart contracts and protocol rules |

| Loan approval | Credit checks, income checks, documents | Collateral value and supported assets |

| Borrower identity | Usually required | Usually wallet-based interaction |

| Collateral | Property, vehicle, guarantees, salary profile | Supported crypto assets |

| Interest rates | Set by lender policy and market conditions | Often changes with supply and demand |

| Enforcement | Legal process and collections | Smart contracts and liquidation rules |

| Main responsibility | Repay according to the loan agreement | Maintain collateral health and repay debt |

This comparison shows why DeFi lending is so interesting.

It does not copy the banking system exactly.

It creates a different type of credit market where collateral, code, liquidity, and price feeds replace many traditional banking processes.

That difference is powerful, but it also means users need to understand how the system works before using it.

A Beginner Story: Thabo Borrows Stablecoins Without Selling ETH

Let us make this practical.

Imagine Thabo owns R20,000 worth of ETH.

He believes ETH may be useful to hold long term, so he does not want to sell it today.

At the same time, he wants R5,000 worth of stablecoins for liquidity.

In a traditional situation, Thabo may have two simple choices.

- Sell some ETH and receive stablecoins.

- Keep the ETH and avoid using that value.

DeFi lending creates a third option.

Thabo may supply ETH as collateral into a DeFi lending protocol and borrow stablecoins against it.

The flow looks like this:

Thabo supplies ETH → ETH becomes collateral → Thabo borrows USDC → interest starts building → Thabo monitors his position → Thabo repays USDC → ETH collateral unlocks.

This is the basic borrowing loop.

Thabo still has exposure to ETH because his ETH is collateral. He also receives stablecoins that he can use elsewhere.

However, this is not free money.

Thabo now has debt.

He must pay interest.

If ETH falls too much, his collateral position can become risky.

If the position becomes too risky, liquidation can happen.

So the practical lesson is simple:

DeFi lending can unlock liquidity from crypto assets, but borrowing creates responsibility.

Why Would Someone Borrow Crypto Instead of Selling?

Beginners often ask a very reasonable question.

If someone needs stablecoins, why not just sell the crypto?

There are several reasons people may borrow instead of selling.

1. They Want Liquidity Without Losing Asset Exposure

A person may believe in the long-term potential of an asset such as ETH or BTC.

Selling the asset gives them liquidity, but it also removes their exposure.

Borrowing against the asset may allow them to access stablecoins while still keeping the original asset as collateral.

This can be useful, but it increases complexity because the borrower now has a loan to manage.

2. They Want Flexibility

Crypto markets move quickly.

Some users borrow stablecoins because they want liquidity available without permanently selling their crypto position.

For example, a user may borrow stablecoins to rebalance, manage cash flow, participate in another DeFi activity, or keep dry powder available.

That flexibility has a cost because borrow interest keeps running.

3. They Want to Avoid Selling at the Wrong Time

A holder may not want to sell during a market dip.

Borrowing can provide temporary liquidity while the asset remains posted as collateral.

This strategy only makes sense if the borrower understands the risks.

If the market keeps falling, the loan can become more dangerous.

4. They May Have Tax or Planning Reasons

In some countries, selling crypto may create a taxable event.

Borrowing may have a different treatment depending on local rules and personal circumstances.

This is not something to guess.

Tax rules differ by country, and readers should get proper guidance where needed.

5. They Use More Advanced DeFi Strategies

Experienced users may borrow to build more advanced strategies across DeFi.

They may use borrowed assets for liquidity provision, hedging, arbitrage, or capital efficiency.

Beginners should not start there.

The first goal is to understand basic supply, borrow, repay, collateral, interest, and liquidation mechanics.

The Core Players in a DeFi Lending Market

A DeFi lending protocol may look complicated from the outside, but the main participants are easy to understand.

Suppliers

Suppliers deposit assets into the lending market.

For example, someone may supply USDC, ETH, or another supported token.

That supplied liquidity becomes available for borrowers, depending on the protocol design.

In return, suppliers may earn interest when borrowers use that liquidity.

Supply rates are not always fixed.

They usually change as market demand changes.

Borrowers

Borrowers take assets from the lending market after supplying enough collateral.

For example, a borrower may supply ETH and borrow USDC.

The borrower pays interest while the loan remains open.

If the collateral value drops too much, the borrower may need to repay part of the loan, add more collateral, or face liquidation.

Liquidators

Liquidators help protect the lending market when a borrower’s position becomes too risky.

If a position crosses the protocol’s risk limits, a liquidator can repay part of the borrower’s debt and receive part of the collateral as an incentive.

This process helps the protocol reduce bad debt.

For the borrower, liquidation can be painful because they lose part of their collateral.

The Protocol

The protocol is the smart contract system that coordinates everything.

It manages deposits, borrowing, repayments, interest rates, collateral rules, liquidations, and market accounting.

Different protocols use different designs.

That is why Aave, Compound, and Morpho all sit inside the DeFi lending category, but they do not work in exactly the same way.

The Supply Side: What Happens When Someone Lends Crypto?

Supplying assets means depositing crypto into a DeFi lending protocol.

For example, Naledi supplies 1,000 USDC into a lending market.

Her USDC adds liquidity to the market.

Borrowers can now access USDC from that pool if they meet the protocol’s collateral rules.

If borrowers pay interest, Naledi may receive a share of that interest as a supplier.

That is the simple version.

However, Naledi’s supply rate can change.

If many borrowers want USDC, the supply rate may rise.

If fewer people borrow USDC, the supply rate may fall.

This is why DeFi lending rates are often dynamic.

They respond to market activity rather than staying fixed like a traditional promotional bank rate.

Simple Supplier Example

| Step | What Happens |

|---|---|

| Step 1 | Naledi supplies 1,000 USDC to a lending protocol. |

| Step 2 | The protocol adds her USDC to the available liquidity market. |

| Step 3 | Borrowers access USDC and pay interest. |

| Step 4 | Naledi may earn a variable supply rate. |

| Step 5 | She can withdraw if liquidity is available and the protocol allows it. |

This is why the supply side often appears in passive income conversations.

Still, it is important to understand that supplying assets is not the same as depositing money into a risk-free account.

The supplier still needs to think about the asset, the protocol, smart contract risk, liquidity, and stablecoin quality.

The Borrow Side: What Happens When Someone Borrows Crypto?

Borrowing means taking assets from a lending market after supplying collateral.

Let us return to Thabo.

He supplies R20,000 worth of ETH as collateral.

The protocol may allow him to borrow a certain amount of USDC, depending on the rules for ETH collateral.

Thabo decides to borrow R5,000 worth of USDC.

At that point, several things are happening:

- His ETH supports the loan.

- His USDC debt starts accumulating interest.

- The protocol tracks the value of his collateral.

- The health of his position changes when ETH moves up or down.

If ETH rises, Thabo’s position may become safer.

If ETH falls, the position becomes riskier.

If ETH falls too far, liquidation may happen.

Simple Borrower Example

| Item | Example Amount |

|---|---|

| Collateral supplied | R20,000 worth of ETH |

| Amount borrowed | R5,000 worth of USDC |

| Borrower goal | Access stablecoin liquidity without selling ETH |

| Main responsibility | Repay debt and keep collateral position healthy |

| Main danger | ETH price falls and the position moves toward liquidation |

This example shows why DeFi borrowing is not casual.

The user is not only clicking a borrow button.

They are managing a live collateralized position.

Collateral: The Heart of DeFi Lending Protocols

Collateral is the asset a borrower supplies to support a loan.

In traditional finance, collateral may be a house, car, business asset, or guarantee.

In DeFi, collateral is usually a crypto asset.

For example, a borrower may use ETH as collateral and borrow USDC.

The protocol decides how much the user can borrow based on the collateral rules.

Not all collateral is treated equally.

A large and liquid asset may receive more favourable terms than a smaller and more volatile token.

That makes sense because the protocol needs confidence that collateral can be valued and sold if liquidation becomes necessary.

Loan-to-Value Explained Simply

Loan-to-value, often called LTV, compares the borrowed amount to the collateral value.

Imagine a user supplies R10,000 worth of ETH.

The protocol may allow borrowing up to R6,000 worth of stablecoins, depending on the rules.

That does not mean borrowing the full R6,000 is wise.

If the ETH price falls, the position can become risky quickly.

A more cautious borrower may borrow only R3,000 or R4,000 to keep a larger safety buffer.

This is one of the most important lessons in DeFi lending protocols:

Maximum borrowing power is not the same as smart borrowing.

Health Factor or Borrow Health

Many lending dashboards show a health metric.

The exact name may differ, but the idea is similar.

A healthier position has more collateral protection.

A weaker position sits closer to liquidation.

Beginners should not ignore this number.

Borrowing is not something to set and forget because market prices can move at any time.

Liquidation Explained Without the Confusion

Liquidation happens when a borrower’s position becomes too risky according to the protocol rules.

Think of liquidation as the protocol protecting the lending market before the loan becomes dangerously undercollateralized.

In a bank loan, a lender may call, send notices, restructure debt, or begin a legal process.

In DeFi, the smart contract follows the rules automatically.

If the collateral value falls too much compared to the debt, liquidators can step in.

A liquidator repays part of the borrower’s debt and receives part of the collateral as an incentive.

This helps protect suppliers and the protocol.

For the borrower, it can mean losing part of their collateral.

Practical Liquidation Example

Imagine Thabo supplies R20,000 worth of ETH and borrows R8,000 worth of USDC.

At first, the position may look comfortable.

Now imagine ETH drops sharply and his collateral value falls from R20,000 to R12,000.

Thabo still owes around R8,000 plus interest.

The loan is now much closer to the danger zone.

If ETH falls further, the protocol may allow liquidation.

To reduce the risk, Thabo may need to repay some USDC, add more ETH as collateral, or close part of the position.

This example shows why borrowers must monitor their positions.

The protocol will not wait for emotions, excuses, or market hopes.

It follows the rules.

Why Stablecoins Matter So Much in DeFi Lending

Stablecoins play a major role in DeFi lending protocols because many borrowers want stable liquidity.

A borrower may not want to borrow another volatile token.

Instead, they may prefer borrowing a stablecoin such as USDC or another supported stable asset.

This creates a common DeFi lending pattern:

- A user supplies a volatile crypto asset as collateral.

- The user borrows a stablecoin.

- The user manages the position over time.

- The user eventually repays the stablecoin debt.

- The collateral becomes available again.

Stablecoins make lending easier to understand because they act like a crypto-native cash layer.

However, stablecoins still need research.

A stablecoin depends on its issuer, reserves, collateral model, redemption process, liquidity, and market confidence.

So even when the borrowed asset looks stable, the stablecoin itself still matters.

How Interest Rates Work in DeFi Lending

Interest rates in DeFi lending protocols usually respond to supply and demand.

When many users want to borrow an asset and fewer users supply it, borrowing can become more expensive.

When there is plenty of supplied liquidity and borrowing demand is low, rates may fall.

The key concept here is utilization.

Utilization Explained With Simple Numbers

Utilization measures how much supplied liquidity is currently being borrowed.

Imagine a USDC lending market has R1,000,000 supplied.

If borrowers have borrowed R500,000, utilization is 50%.

If borrowers have borrowed R900,000, utilization is 90%.

Higher utilization often pushes borrow rates higher because available liquidity becomes tighter.

Lower utilization usually means there is more unused liquidity, so borrow rates may be lower.

Why Utilization Matters

Utilization affects both suppliers and borrowers.

Borrowers care because high utilization can make loans more expensive.

Suppliers care because strong borrowing demand can increase the interest they may earn.

However, very high utilization can also make the market less comfortable.

If too much liquidity is borrowed, suppliers may find withdrawals harder because less liquidity remains available.

Healthy lending markets need balance.

Too little borrowing demand can make supplier yields low.

Too much borrowing demand can make the market tight.

Aave, Compound and Morpho: Three DeFi Lending Examples

There are many DeFi lending protocols, but Aave, Compound, and Morpho are useful examples because they show how the lending sector has developed.

This section is not about ranking them.

It is about helping beginners understand different lending designs.

Aave: Shared Liquidity Markets

Aave is one of the best-known DeFi lending protocols.

Its model allows users to supply assets into liquidity markets and borrow supported assets against collateral.

Aave’s official documentation describes it as a decentralised non-custodial liquidity protocol where users can participate as suppliers or borrowers. You can read the official overview here: Aave Protocol documentation.

For beginners, Aave is useful to study because it shows the classic DeFi money market model.

Users supply assets, borrowers access liquidity, and interest rates respond to market conditions.

The important beginner lesson is simple:

Aave shows how DeFi can create shared lending markets through smart contracts.

Compound: Base Asset Borrowing

Compound is another major DeFi lending protocol.

Compound III uses a model where users supply collateral to borrow a base asset.

The official Compound documentation explains that Compound III enables users to supply crypto assets as collateral in order to borrow the base asset, while accounts can earn interest by supplying the base asset to the protocol. You can read the documentation here: Compound III documentation.

For beginners, Compound is useful because it shows that not every lending protocol uses the same design.

The broad idea may be similar, but the details matter.

Morpho: More Modular Lending Infrastructure

Morpho is another important DeFi lending example because it shows how the sector continues to evolve.

Morpho’s documentation describes the Morpho Protocol as a decentralized, noncustodial lending protocol implemented for the Ethereum Virtual Machine. You can read the official learning page here: Morpho documentation.

Morpho is often discussed as lending infrastructure rather than only a simple supply-and-borrow app.

Its ecosystem can involve markets, vaults, curators, and more flexible ways to allocate liquidity.

For beginners, the key lesson is not to memorize every technical detail immediately.

The key lesson is that DeFi lending is becoming more modular.

Simple Comparison: Aave vs Compound vs Morpho

The table below gives a simplified beginner view.

It is not a full technical comparison and should not be used as an investment decision tool.

Rather, it helps readers understand how these protocols differ conceptually.

| Protocol | Beginner View | What It Helps You Understand | Key Learning Point |

|---|---|---|---|

| Aave | Shared liquidity markets for supplying and borrowing | Classic DeFi lending, collateral, borrowing, and liquidity pools | DeFi can coordinate lenders and borrowers through smart contracts. |

| Compound | Base asset borrowing model in Compound III | How collateral can support borrowing of a specific base asset | Protocol design choices affect how lending markets behave. |

| Morpho | More modular lending infrastructure | Markets, vaults, curators, and flexible lending design | DeFi lending is evolving beyond one-size-fits-all pools. |

Beginners do not need to master every protocol immediately.

A better approach is to understand the concepts first.

Once the concepts are clear, protocol differences become easier to study.

How to Read a DeFi Lending Dashboard

A DeFi lending dashboard can look intimidating the first time you see it.

There may be APYs, borrow rates, collateral toggles, health factors, liquidation thresholds, available liquidity, and wallet balances.

Once you know what to look for, the dashboard becomes easier to understand.

Supply APY

Supply APY shows the estimated yearly return suppliers may earn by depositing an asset.

This number can change because borrowing demand changes.

If more people borrow the asset, the supply APY may rise.

If fewer people borrow it, the supply APY may fall.

Borrow APR

Borrow APR shows the estimated cost of borrowing an asset.

This rate can also change over time.

Borrowers should not assume the rate will stay the same forever.

Available Liquidity

Available liquidity shows how much of an asset remains available in the market.

If liquidity is low, withdrawals or borrowing may become less comfortable.

This number helps users understand how much unused liquidity remains.

Collateral Toggle

Some dashboards allow users to choose whether a supplied asset can be used as collateral.

Turning collateral on may allow borrowing.

Turning it off may reduce borrowing ability but can also reduce certain risks depending on the protocol.

Liquidation Threshold

The liquidation threshold helps determine when a borrowing position becomes risky enough for liquidation.

Borrowers should understand this before taking a loan.

It is one of the most important numbers on the dashboard.

Health Factor

The health factor shows how safe or risky a borrowing position is.

A stronger health factor means the position has more breathing room.

A weaker health factor means the position is closer to liquidation.

Net APY or Net Position

Some dashboards show a net figure that combines supply earnings and borrowing costs.

This can help users see whether their overall position is costing them money or earning something after both sides are considered.

Beginners should not rely on one dashboard number alone.

They should understand what each number means.

A Beginner Dashboard Walkthrough

Imagine Lerato opens a lending dashboard for the first time.

She sees two main sections: supply and borrow.

Under supply, she sees USDC with a supply APY of 4%.

Under borrow, she sees USDC with a borrow APR of 7%.

At first, she may wonder why the borrow rate is higher than the supply rate.

The reason is that borrowers pay interest, suppliers receive interest, and the protocol’s interest model may include spreads, reserves, or other mechanics depending on the design.

Then Lerato checks available liquidity.

If plenty of USDC remains available, the market may feel comfortable.

If most USDC has already been borrowed, utilization may be high and rates may increase.

Next, she checks collateral options.

She sees that ETH can be used as collateral, but a smaller volatile token cannot.

This teaches her that lending protocols do not treat every asset the same.

Finally, she studies the health factor.

She learns that if she borrows, this number becomes important because it shows how close her position may be to liquidation.

This simple walkthrough gives a beginner a practical way to read a lending dashboard without feeling lost.

Why DeFi Lending Is Useful

DeFi lending is useful because it creates open financial markets that operate on-chain.

Users can supply liquidity.

Borrowers can access liquidity.

Smart contracts coordinate the rules.

On-chain data can make parts of the market visible.

This is very different from traditional finance, where many internal processes remain hidden from ordinary users.

In DeFi, users can often inspect supplied liquidity, borrowed amounts, interest rates, liquidations, supported collateral, and protocol activity using dashboards, block explorers, and analytics tools.

That transparency is one of DeFi’s strongest features.

However, visible does not always mean easy.

Beginners still need to learn how to read the data.

This is where the Best On-Chain Crypto Tools guide can help readers build stronger research habits.

Why DeFi Lending Can Be Difficult

DeFi lending can also be difficult because several moving parts operate at the same time.

A user needs to understand the asset, protocol, wallet, network fees, interest rates, collateral settings, liquidation rules, smart contracts, price oracles, and market volatility.

That is a lot for a beginner.

DeFi also does not usually offer the same support experience as a bank.

If a user signs the wrong transaction, the blockchain may not reverse it.

If collateral gets liquidated, the protocol follows the rules.

If funds move on the wrong network, recovery may be difficult or impossible.

This does not make DeFi bad.

It means DeFi requires education.

That is why beginner-friendly explanations matter.

Important DeFi Lending Terms Beginners Should Know

DeFi lending becomes much easier once the basic vocabulary makes sense.

Supply

To supply means to deposit an asset into a lending protocol.

Borrow

To borrow means to take an asset from the protocol after meeting collateral requirements.

Collateral

Collateral is the asset supplied to support a loan.

Loan-to-Value

Loan-to-value compares the borrowed amount to the collateral value.

Liquidation

Liquidation happens when the protocol allows a risky borrowing position to be partially or fully closed by liquidators.

Utilization

Utilization measures how much supplied liquidity has been borrowed.

Supply APY

Supply APY shows the estimated yearly return suppliers may earn, although rates can change.

Borrow APR

Borrow APR shows the estimated interest cost borrowers may pay, although rates can also change.

Oracle

An oracle provides external price information to the protocol.

Health Factor

A health factor, or similar metric, shows how safe or risky a borrowing position is relative to liquidation.

These terms are the foundation.

Once they make sense, DeFi lending protocols become much easier to understand.

How DeFi Lending Connects to Passive Income

DeFi lending connects to passive income mainly through the supply side.

When users supply assets into a lending market, they may earn interest if borrowers use that liquidity.

This is why lending protocols often appear in crypto passive income conversations.

However, the deeper lesson is bigger than yield.

Supplying assets is not just about earning a displayed APY.

The return comes from a market process.

Borrowers pay interest.

The protocol coordinates liquidity.

Collateral supports the loans.

Liquidators help protect the market.

Interest rates respond to supply and demand.

That whole system creates the lending environment.

So the income side is only one part of the story.

The deeper point is that DeFi lending protocols are crypto-native credit markets.

A Beginner Learning Path for DeFi Lending Protocols

Beginners do not need to rush into using DeFi lending protocols with real money.

A better learning path starts with understanding the system first.

Step 1: Learn the Vocabulary

Start with supply, borrow, collateral, liquidation, utilization, APY, APR, oracle, and health factor.

If those terms are confusing, the protocol interface will feel confusing too.

Step 2: Study One Protocol at a Time

Choose one protocol to study first.

Read the official documentation.

Open the interface without connecting funds.

Look at the markets, rates, supported assets, and collateral settings.

The goal is to understand the screen before taking any action.

Step 3: Watch the Market Without Depositing

Observe supply rates, borrow rates, available liquidity, utilization, and collateral settings over time.

This helps you see that DeFi lending markets move.

Step 4: Study Liquidation Examples

Liquidation is one of the most important concepts in DeFi lending.

Beginners should understand how a healthy position can become risky when collateral value falls.

Step 5: Use Testnets or Tiny Amounts for Learning

Where possible, use test environments, simulations, or very small amounts for learning.

The goal is not to chase returns.

The goal is to understand the mechanics.

Step 6: Build a Risk Checklist

Before using any DeFi lending protocol seriously, build a checklist.

Check the protocol, asset, collateral, interest rate, liquidation rules, smart contract risk, wallet security, and exit plan.

The 10-Step DeFi Safety Checklist is a useful place to start.

Common Beginner Mistakes With DeFi Lending

DeFi lending can be educational and useful, but beginners often make mistakes when they move too quickly.

Mistake 1: Borrowing Too Close to the Limit

Borrowing the maximum allowed amount can leave very little room for market movement.

If collateral falls, liquidation can happen quickly.

A larger safety buffer gives the borrower more room to react.

Mistake 2: Ignoring Borrow Rates

Borrow rates can change.

A loan that looks affordable today may become more expensive if market conditions shift.

Borrowers should monitor rates instead of assuming they stay fixed.

Mistake 3: Treating Stablecoins as Risk-Free

Stablecoins are useful, but they are not magic.

They depend on design, reserves, collateral, liquidity, redemption, and market confidence.

Mistake 4: Not Understanding Liquidation

Liquidation is not a small detail.

It is central to how DeFi lending protects the market.

Any borrower should understand liquidation before opening a position.

Mistake 5: Using Too Many Protocols Too Soon

Jumping between several protocols can make risk harder to track.

Beginners should learn slowly and build confidence before exploring more advanced systems.

Mistake 6: Forgetting Network Fees

Every action on-chain may require transaction fees.

Supplying, borrowing, repaying, withdrawing, adding collateral, and adjusting a position may all require network fees.

Fees can matter, especially for small amounts.

How DeFi Lending Fits Into the Bigger Crypto Picture

DeFi lending is not an isolated niche.

It connects to many parts of the crypto market.

Stablecoins matter because borrowers often want stable liquidity.

Decentralized exchanges matter because traders and liquidity providers may use borrowed assets in different strategies.

On-chain analytics matter because lending activity can reveal how capital moves through markets.

Real-world assets may connect with lending when tokenized credit markets develop.

Wallets and custody tools matter because users need safe ways to interact with protocols.

In other words, DeFi lending is part of crypto’s financial plumbing.

It may not always be the loudest topic, but it is one of the most important to understand.

The Simple Passive Income Approach

At SPI, the goal is not to make crypto sound easy.

The goal is to make crypto easier to understand.

DeFi lending protocols are a perfect example.

On the surface, they may look like simple earn-and-borrow platforms.

Underneath, they are on-chain credit markets powered by collateral, liquidity, interest rate models, price oracles, smart contracts, and liquidation systems.

That makes them worth studying even if you are not ready to use them.

Understanding DeFi lending helps beginners think better about passive income, stablecoins, crypto borrowing, and protocol design.

It also helps experienced crypto users explain the market more clearly to others.

The best approach is simple:

- Learn the vocabulary first.

- Understand why people borrow.

- Study how collateral protects the system.

- Watch how interest rates respond to demand.

- Respect liquidation rules.

- Research protocols before using them.

That is how DeFi becomes less confusing and more useful.

Final Thoughts

DeFi lending protocols are one of the clearest examples of how crypto is building financial infrastructure outside the traditional banking system.

They allow users to supply assets, borrow against collateral, repay loans, and participate in on-chain money markets.

Protocols like Aave, Compound, and Morpho show that DeFi lending can take different forms, from shared liquidity markets to base asset borrowing models and more modular lending infrastructure.

For beginners, the most important lesson is not to chase yield or borrow quickly.

The better first step is to understand the machine.

Who supplies liquidity?

Who borrows it?

What collateral supports the loan?

How does the interest rate move?

When can liquidation happen?

How does the protocol stay solvent?

Those questions help you see DeFi lending as more than an app screen.

They reveal the structure behind the market.

Once you understand that structure, you can study crypto with more confidence, more patience, and more clarity.

DeFi lending is not just about earning interest. It is about understanding how crypto-native credit markets work.

Leave a Reply