Inflation — how it works — is one of the most important financial concepts most people misunderstand.

You might think your money is safe sitting in your account.

However, over time, inflation quietly reduces what your money can actually buy.

In other words, even if your balance stays the same, your purchasing power is slowly shrinking.

This guide explains inflation, how it works, and what you can do to protect your money in the real world.

The Invisible Problem: Losing Value Without Noticing

At first, inflation does not feel like a problem.

There is no alert. No sudden loss. No visible deduction from your account.

Instead, the impact shows up in everyday life.

Groceries cost more than they did last year.

Fuel prices increase.

Rent rises.

Basic living expenses slowly creep upward.

Because these changes happen gradually, many people underestimate how powerful inflation really is.

However, over time, the effect compounds.

As a result, your money buys less and less — even if your income has not changed.

What Inflation Is and How It Works

So, what is inflation?

Simply put, inflation is the rate at which prices increase over time.

If inflation is 5% per year, something that costs $100 today will cost about $105 next year.

That may seem small.

However, inflation compounds — just like investing does.

Because of this, small annual increases turn into significant long-term changes.

This is why central banks, including the Federal Reserve and the South African Reserve Bank, closely monitor inflation levels.

In many countries, a moderate level of inflation is considered normal.

However, when inflation rises too quickly, it begins to erode wealth at a much faster rate.

A Real Example of Inflation and How It Works

Let’s make this practical.

Imagine you have $1,000 sitting in cash.

If inflation averages 5% per year, your purchasing power changes like this:

- After 1 year → ~$950 in real value

- After 5 years → ~$780

- After 10 years → ~$600

Your bank balance still says $1,000.

However, what that money can actually buy has dropped significantly.

In countries where inflation is higher, this effect becomes even more pronounced.

As a result, holding large amounts of cash for long periods can quietly reduce your wealth.

Why Inflation Makes Saving Money Alone Risky

Saving money is important.

It provides stability, security, and flexibility.

However, saving alone is not a complete financial strategy.

Here’s why.

If your savings earn 2–3% interest, but inflation is 5%, your money is losing value in real terms.

This is known as a negative real return.

In other words, your money is growing in numbers — but shrinking in purchasing power.

Because of this, relying only on savings can create a false sense of security.

If you want to structure your money properly, this guide explains how to decide how much cash you should keep while still investing effectively.

Want More Simple, Practical Financial Breakdowns?

If you’re serious about building real wealth — not just saving money — the Simple Passive Income newsletter shares practical strategies, investing frameworks, and step-by-step guides.

This is the point where most readers realise they need a better system, which makes it the ideal place to add your signup form.

Who Inflation Hurts the Most

Although inflation affects everyone, it impacts some groups more than others.

For example:

- People holding large amounts of cash

- Individuals without investments

- Low-growth income earners

- Those relying only on savings accounts

In economies with higher inflation rates, the impact becomes even more noticeable.

Therefore, understanding inflation is not optional — it is essential.

How to Protect Yourself From Inflation

The solution is not complicated.

However, it does require a shift in thinking.

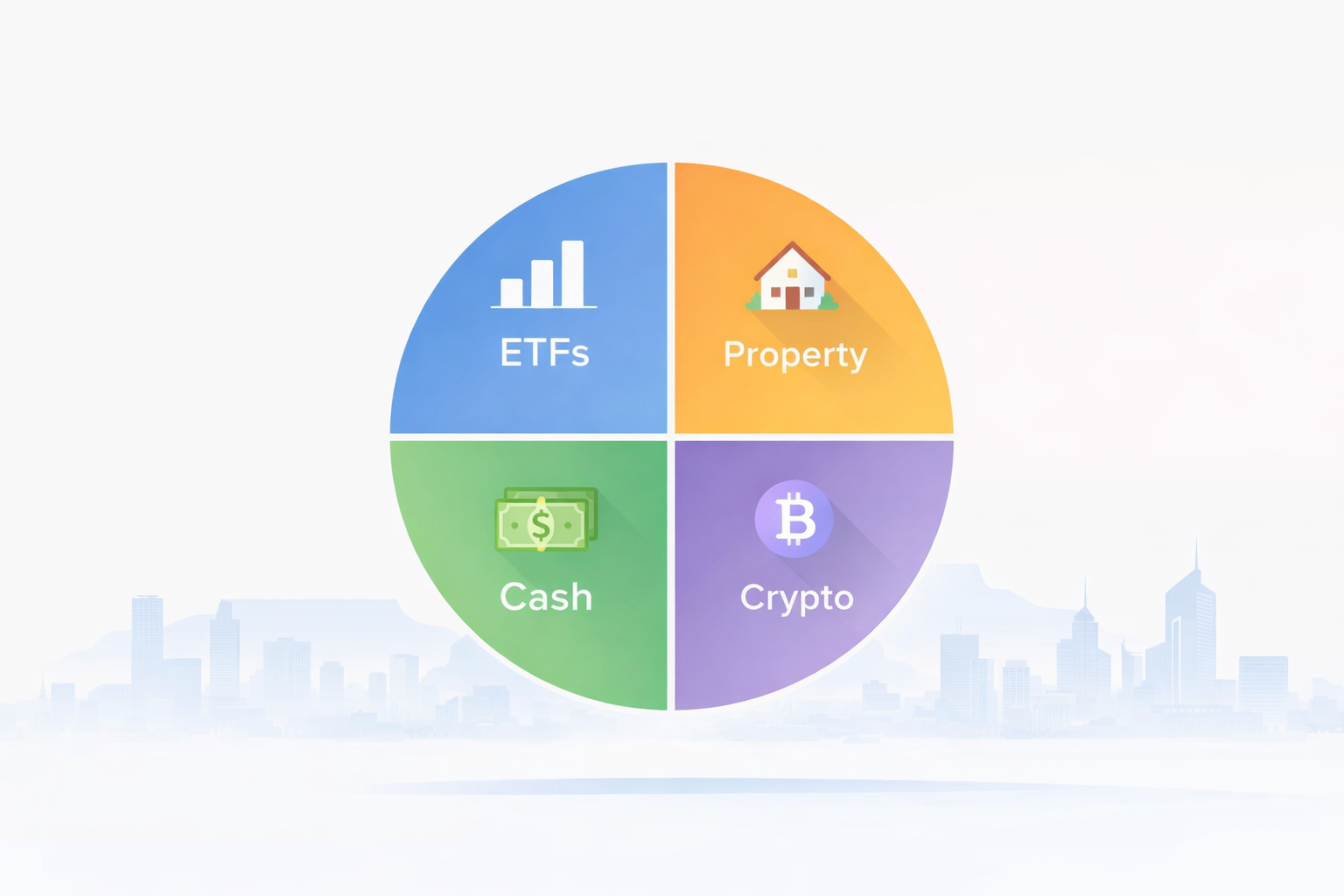

Instead of only saving money, you need to allocate capital into assets that can grow over time.

1. Invest in Stocks and ETFs

Equities have historically outpaced inflation over the long term.

They represent ownership in businesses that can grow, raise prices, and increase profits.

If you want a structured approach, this guide explains how to build a simple investment portfolio.

2. Consider Property and Real Assets

Property often increases in value alongside inflation.

Additionally, rental income can rise over time, helping offset increasing costs.

3. Build Passive Income Streams

Income-generating assets can help you stay ahead of rising expenses.

If you want to explore this further, this guide explains how to build passive income in a practical way.

4. Diversify Your Investments

Rather than relying on a single asset, spreading your investments across multiple areas improves stability and reduces risk.

This approach helps protect your portfolio against different economic conditions.

What Most People Get Wrong About Inflation

Many people misunderstand how inflation works.

As a result, they make avoidable mistakes.

For example:

- They believe saving is enough

- They delay investing for too long

- They underestimate compounding

- They hold too much idle cash

Over time, these decisions allow inflation to quietly erode wealth.

A Simple Anti-Inflation Plan

If you want a practical approach, here is a simple framework:

Step 1: Build an emergency fund

Step 2: Invest consistently over time

Step 3: Focus on long-term growth assets

Step 4: Diversify your portfolio

Step 5: Stay consistent and avoid emotional decisions

This approach does not depend on perfect timing.

Instead, it relies on consistency and discipline.

How Inflation Connects to Your Bigger Financial Strategy

Inflation is not just a theory.

It directly affects every part of your financial life.

For example:

- Your investment portfolio

- Your passive income strategy

- Your long-term retirement planning

If you ignore inflation, your financial strategy weakens over time.

However, if you understand inflation and respond correctly, your strategy becomes significantly stronger.

Final Thoughts

Inflation is quiet.

It does not feel urgent.

It does not create panic.

However, over time, it can have one of the biggest impacts on your wealth.

The goal is not to fear inflation.

Instead, the goal is to understand how inflation works — and respond intelligently.

Start building assets.

Stay consistent.

Think long term.

Because the real risk is not losing money overnight.

It’s losing value slowly without realising it.

Leave a Reply